June 2026 Monthly Investment Update

Source: Blueprint Investment Partners

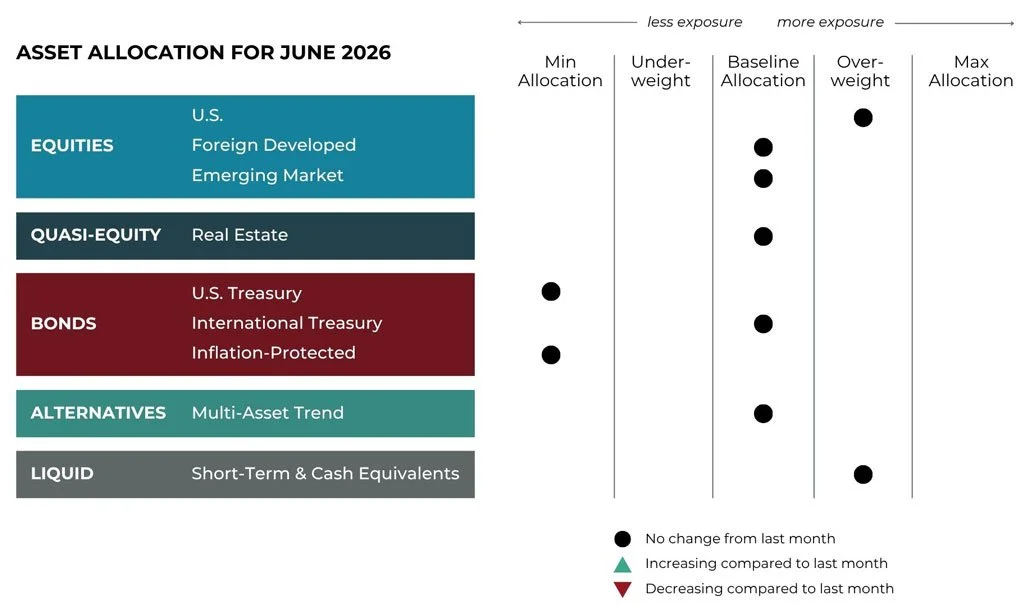

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will not change and remain overweight. Both the intermediate-term and long-term trends are positive.

International Equities

Exposure will not change and remain at baseline. Both foreign developed and emerging market equities have intermediate- and long-term uptrends.

Real Estate

Exposure will remain at its baseline allocation as trends over both timeframes remain positive.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for continued baseline exposure and offer the ability to potentially benefit from both positive and negative trends. U.S. Treasuries of medium to long duration remain in downtrends across all timeframes and will continue to be underweight.

Inflation-Protected Bonds

Exposure will remain at its minimum as this asset group continues to be weaker than other fixed income assets.

Alternatives

Exposure is expressed through a multi-asset alternative ETF. Fixed income continues to have the largest net exposure (short prices, long rates). Net long equities remains in the second spot as the largest long position. International currencies and commodities round out the exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will not change and be overweight as this asset class continues to hold allocations from weaker fixed-income instruments.

MONTLHY NOTE

These Are Not Synonyms: Information & Signal

“The problem with experts is that they do not know what they do not know.”

– Nassim Taleb

Most investors today do not suffer from a lack of information. They suffer from too much of it.

Headlines arrive instantly. Opinions multiply by the minute. Every economic release, policy debate, and geopolitical development gets dissected in real time across an expanding number of channels.

The question is no longer where to find market commentary but which commentary or opinion, if any, deserves a response.

The month of May was a useful illustration. Markets navigated inflation concerns, shifting rate expectations, geopolitical tension, fiscal debates, and ongoing questions about artificial intelligence and concentration risk. Underlying trends largely persisted through the noise. The gap between what headlines suggested and what markets actually did was notable, though not unusual.

This month's Note explores the distinction between information and signal, why short-term activity often feels more important than it is, and how a systematic investing process helps separate temporary noise from lasting change.

But first, here’s a summary of what transpired in the markets in May.

Asset-Level Overview

Equities & Real Estate

Uncertainty in the Middle East, energy prices, and inflation remain the dominant factors impacting equity markets. Despite these risks, the S&P 500 moved higher in May, expanding on April’s rally and making new all-time highs once again. The result is that trends remain positive and our portfolios will continue to be overweight.

International equities were more mixed in May, with developed markets joining U.S. markets moving higher and emerging markets trailing the other two. This divergence has allowed U.S. performance to close the gap year-to-date, but international equities continue to outperform. Trends remain solidly positive, which will allow our portfolios to maintain their current allocations.

Real estate security returns were on the muted side in May, with performance currently sitting slightly positive for the month. With renewed inflation concerns pushing lending rates higher, this segment is facing a significant headwind. A new Federal Reserve Chair is yet another factor contributing to uncertainty for this asset class.

Fixed Income & Alternatives

Speaking of asset classes affected by inflation and monetary policy uncertainty, fixed income instruments continued to mostly struggle in May. Pressure on rates to rise has driven bond prices lower across all durations. The result is that our portfolios will remain at their minimum allocations in favor of money market instruments.

Within the alternatives allocation very little change has occurred as we transition to June. Sustained equity trends will keep the equity allocation high while interest rate support described above will keep major short positions in place for fixed income instruments. Elevated oil prices will once again hold the commodity allocation net long while the net long to international currencies will be virtually unchanged.

Sourcing in this section: fortune.com, “S&P 500 sets all-time high, welcomes another company to $1 trillion market cap club,” 5/27/2026

3 Potential Catalysts for Trend Changes

Inflation Rising:

The Fed’s preferred gauge of monthly price increases grew more slowly in April. However, it remained higher than the Fed’s ideal target. The personal-consumption expenditures (PCE) price index rose 0.4% in April versus the previous month, and it rose 0.7% in March. During the past year, the index increased 3.8%, which is higher than the Fed's 2% target. The core 12-month PCE inflation rate is 3.3%. Compared to a year ago, energy prices rose 18%, gasoline 28%, fuel oil 54%, and airfare prices 21%. The latest report means that the rate cuts the market expected at the start of the year are no longer a 2026 story. Four months ago, the Federal Reserve was considering whether to keep cutting interest rates to help a shaky labor market. Now, with inflation data being so critical, the Fed’s policy debate has shifted from when to cut rates to when to signal that a rate hike is as likely as a rate cut.

Consumer Confusion:

Consumers are the cornerstone of the American economy. So far, their spending has held up well in 2026 despite higher prices and slow labor-market hiring. For example, retail sales grew by 0.5% in April. Yet, in economic surveys, Americans report one of the grimmest moods on record. On the other hand, the stock market doesn't seem to be reflecting a sour outlook. Last week, the S&P 500 logged its eighth-consecutive week higher.

Ongoing Housing Squeeze:

U.S. home-price growth slowed slightly in March, during a time when higher mortgage rates intensified the affordability squeeze for home buyers. A measure of home prices across the country, S&P Case-Shiller National Home Price Index, increased 0.7% in the 12 months through March versus a 0.8% rise in February. Mortgage rates also recently hit the highest level since August (6.51% for a 30-year fixed). Mortgage rates usually loosely track 10-year Treasury yields, which have risen following high inflation data. The combination of prices, rates, and other factors spells bad news for home shoppers and coincides with what is usually the busiest time of year for home sales. A fourth-straight slow year for the housing market will also be a challenge for industries that rely on home sales, such as real-estate brokerages, mortgage lenders, home builders, and furniture manufacturers.

Sourcing for this section: The Wall Street Journal, “Iran War Keeps Fed’s Inflation Gauge Above Inflation Target,” 5/28/2026; The Wall Street Journal, “Inflation Soared to 3.8% in April, Driven by Gasoline Prices,” 5/12/2026; The Wall Street Journal, “Retailers’ Sales Growth Cooled Last Month,” 5/14/2026; finance.yahoo.com, “S&P 500 eyes 8th straight weekly gain amid Iran deal hopes,” 5/22/206; The Wall Street Journal, “U.S. Home Price Growth Slowed in March,” 5/26/2026; and The Wall Street Journal, “Mortgage Rates Hit a Nine-Month High in Blow to Prime Buying Season,” 5/21/2026

Information is Flowing Faster, But Trends Usually Are Not

“In the short run, the market is a voting machine but in the long run it is a weighing machine.”

– Benjamin Graham

If you followed financial headlines during May, you would be forgiven for thinking markets had every reason to struggle. Investors navigated persistent inflation concerns, shifting expectations around interest rates, geopolitical uncertainty, fiscal debates, questions surrounding global growth, and the constant drumbeat of election-related noise around the world. On top of that, developments in artificial intelligence continued creating excitement in some corners of the market while simultaneously raising concerns about concentration risk and valuations in others.

The modern investor has access to more information than at any point in history. News alerts arrive instantly. Market commentary appears by the minute. Social media amplifies every opinion, prediction, and short-term market move. Information moves faster than ever before. The interesting thing is that trends generally do not.

One of the core principles behind systematic trend following is recognizing that markets often experience temporary volatility (both up and down) without experiencing a meaningful change in direction. A sharp move over several trading sessions may feel important at the moment. A concerning headline may create anxiety. An unexpected economic report may dominate conversations for days. But short-term activity and long-term trend change are not always the same thing.

Investors frequently face a difficult behavioral challenge: separating information from noise. When headlines arrive continuously, it becomes tempting to react continuously. Yet history has repeatedly shown that frequent reactions can create more problems than they solve. As the quote above from legendary investor Benjamin Graham observes: daily sentiment, emotion, and headlines can influence short-term outcomes, but sustained trends tend to reflect larger underlying forces over time.

This distinction matters because successful investing is not simply about gathering information. It is about identifying which information deserves action. Trend following does not attempt to predict inflation readings, forecast central bank decisions, estimate election outcomes, or anticipate geopolitical developments. Those variables matter, but markets often process them long before consensus opinion catches up.

Instead, systematic trend following focuses on a different set of questions:

What is happening?

Is it persistent?

Does portfolio positioning need to adapt?

That discipline becomes especially valuable during environments like today, where information flow can create the illusion that every development requires immediate action. Sometimes trends change quickly. Risk management exists for precisely that reason. But many times, markets demonstrate resilience even while headlines suggest instability. Strong trends can persist longer than investors expect. Weak trends can deteriorate further than forecasts predict.

Our systematic investing process exists to reduce the temptation to confuse motion with direction. Headlines will continue moving faster than trends. They generally always have. The goal is not to ignore information. The goal is to maintain the discipline to distinguish between temporary noise and lasting change. Because over time, successful investing is often less about reacting faster and more about reacting better.

Important Information:

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy or of any particular strategy or investment product. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. The above commentary is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Not intended as legal or investment advice or a recommendation of any particular security or strategy.

Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from MIller Wealth Partners.

An index is an unmanaged portfolio of specific securities. The performance of which is often used as a benchmark in judging the relative performance of certain asset classes. It should not be assumed that past performance in any way relates to future results. An investment cannot be made directly in an index. An index does not charge management fees or brokerage expenses, and no such fees or expenses were deducted from the performance shown.

S&P 500 Index: A widely used U.S. equity benchmark. It contains 500 U.S. stocks chosen for market size, liquidity, and industry group representation.