May 2026 Monthly Investment Update

Source: Blueprint Investment Partners

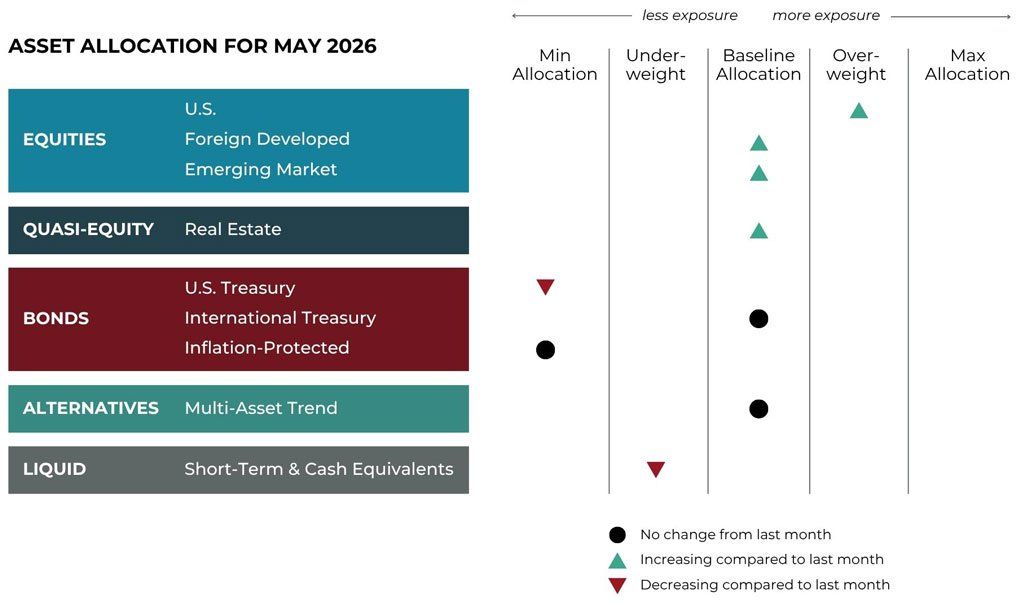

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will increase and move to overweight. The intermediate-term trend has resumed its positive direction, joining the long-term trend.

International Equities

Exposure will increase to baseline. Both foreign developed and emerging market equities have intermediate-term uptrends. Trends continue to be positive over the long-term timeframe as well.

Real Estate

Exposure will increase back to its baseline allocation as trends over both timeframes revert to positive.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for continued baseline exposure and offer the ability to potentially benefit from both positive and negative trends. However, U.S. Treasuries of medium to long duration continue to experience downtrends over both timeframes and will remain underweight.

Inflation-Protected Bonds

Exposure will remain at its minimum as it continues to be weaker than other fixed income assets.

Alternatives

Exposure is expressed through a multi-asset alternative ETF and is overall little changed heading into May. Fixed income will continue to have the largest net exposure (short prices, long rates). Net long equities remain in the second spot and is the largest long position. International currencies and commodities will again bring up the rear in terms of exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will decrease to underweight as exposure is returned to strengthening equities.

MONTLHY NOTE

A Trend Follower Walks Into a V-Shaped Recovery

“The greatest liberty is born of the greatest rigor.”

– Paul Valéry

The market environment over the past several weeks has been defined by speed. A sharp equity drawdown was followed by an equally rapid recovery, creating a difficult backdrop for many investors and particularly for systematic investing strategies.

In periods like this, price tends to move faster than fundamentals can be interpreted or acted upon. By the time a narrative takes shape, markets have often already moved in the opposite direction.

Moves like these can feel disorienting, as conditions change faster than most investing approaches are designed to fully capture. They also tend to expose the tradeoffs embedded in different approaches — especially those that rely on price and discipline rather than prediction.

This month’s Note examines how our trend-following process has evolved to better navigate these environments and how those refinements influenced positioning through the recent volatility.

But first, here’s a summary of what transpired in the markets in April.

Asset-Level Overview

Equities & Real Estate

While no sustainable solution has been reached yet, the temporary ceasefire and its subsequent extension in Iran has been the catalyst for a massive rally in equities back to new highs within the span of just a couple weeks. As we mentioned in last month’s update, an otherwise strong economy is likely providing the foundation for a continuation of positive trends once uncertainty in the Middle East abates. This appears to be the case thus far as April draws to a close.

International equities have also benefited from the temporary cooling of tensions as negotiations continue. Productive discussions mean lower oil prices, which means less pressure on inflation to continue. This in turn opens the door for favorable monetary policy.

Last but not least to benefit from the temporary ceasefire are real estate securities. Like their other equity counterparts, the hint of stable interest rates have allowed them to resume the uptrends they had started going into April.

The result is that our portfolios will increase exposure in all these areas.

Fixed Income & Alternatives

Many of the same catalysts driving equity markets are also influencing fixed income, albeit in different ways. After the prospect of a spike in inflation drove rates higher and prices lower, a pause in the intensity of the war has allowed prices to stabilize. Interestingly, bond prices have not recovered anywhere near what equity prices have; in some cases they have been flat to lower. This raises the question of what else is driving bond markets. Perhaps it is the grilling of the new Fed Chair candidate? Who knows, but for now prices remain weak enough that no new uptrends have emerged.

Within the alternatives allocation, the recovery in equity prices will keep the equity allocation high. Elevated oil prices will keep the commodity allocation net long while the net long to international currencies will be subdued. Last but not least, the fixed income allocation will continue to be net short but poised to change quickly if bond prices recover.

3 Potential Catalysts for Trend Changes

Sentiment Matters:

Concerns about the war in Iran have led Americans to their most pessimistic economic outlook on record, according to the University of Michigan’s long-running consumer sentiment survey. The index fell to 49.8 in May from 53.3 in April, below the previous record low of 50 set in June 2022. A preliminary April reading of 47.6 had already indicated worsening sentiment. Notably, Americans now feel worse about the economy than during the COVID-19 pandemic, the 2008-2009 Financial Crisis, or the high inflation period of the late 1970s. Despite this pessimism, consumer spending has remained relatively stable. While April data is pending, March retail sales were strong, and major banks report that household finances are solid. As for unemployment expectations, which economists have tracked since the 1960s, pessimism during the past year has risen and matched levels typically seen only during recessions. In March, both the New York Fed and the Conference Board reported increased consumer negative sentiment. An April poll by the Associated Press-NORC Center for Public Affairs Research found that 73% of Americans believe the economy is performing poorly. Never before have so many expected unemployment to rise without an actual recession. This unusual labor market likely reflects limited hiring and firing, fewer available workers due to immigration restrictions, and uncertainty about the effects of artificial intelligence.

Pricing Expectations:

The Labor Department reported that consumer prices rose 3.3% in March compared to a year earlier, up from 2.4% in February. This is the highest inflation rate in two years, though it met economists' expectations. At his final Federal Reserve meeting as Chairman, Jerome Powell cautioned that inflation is likely to continue rising in the coming months. “It hasn’t even peaked yet,” Powell stated at a press conference on Wednesday. “There’s headline inflation coming out of the Gulf, and we don’t know how much that will be.” Core inflation, which excludes food and energy, increased by 2.6%, just below the 2.7% forecast. Consumers are reducing purchases in categories with the largest price increases, indicating that company price hikes, rather than strong demand, are driving inflation. While Americans continue to spend, aided by tax refunds, their purchasing patterns are shifting. Spending on clothing, furniture, and sports equipment has declined as these items have become more expensive, while spending on services and experiences, such as travel and healthcare, has increased. Bureau of Economic Analysis data through February shows that inflation-adjusted spending is falling most for goods with the highest price increases. Overall, consumer spending remains steady, suggesting inflation’s impact may be limited, even as many express concern.

Powell’s Last Dance:

For 75 years, every Federal Reserve Chair has left the central bank when a successor was appointed. Powell has broken this tradition by announcing he will remain on the Fed’s board as a Governor after transferring leadership to Kevin Warsh in May. This decision reflects the significant influence of the President Donald Trump administration on the Fed’s operations. Powell’s announcement followed a criminal investigation into his management of building renovations, and although Trump supported the investigation, prosecutors ended it last week to facilitate Warsh’s confirmation. Warsh’s nomination advanced in the Senate Banking Committee along party lines, marking the first time a Fed Chair was approved without bipartisan support. Other Fed tensions arose following the decision to leave rates unchanged during the April meeting. Three regional Presidents publicly disagreed with Powell, not on the most recent rate decision itself, but on the message that a rate cut is more likely than a hike. The three Presidents were effectively putting Warsh on notice that with rising energy prices, inflation near 3%, and ongoing tariffs, they do not believe the Fed can deliver the rate cuts sought by the White House. A fourth dissent expressed desiring a rate cut rather than keeping the rate unchanged. The four dissents at the April meeting were the most since 1992, before the Fed began announcing rate decisions in real time. The central bank’s next meeting is scheduled for June 16-17.

Sourcing for this section: The Wall Street Journal, “April’s Consumer Sentiment Is the Lowest on Record,” 4/24/2026; The Wall Street Journal, “Most Americans Think the Job Market Will Get Worse. Here’s Why That Matters.,” 4/24/2026; The Wall Street Journal, “Inflation Soared to 3.3% in March, Driven by Higher Gasoline Costs,” 4/10/2026; and The Wall Street Journal, “Powell Won’t Leave. The Fed Won’t Cut. Warsh Will Have to Deal With Both.,” 4/29/2026

Evolving Thoughtfully, Staying Disciplined, Letting Trends Guide The Way

“To be a successful investor, you have to have a philosophy and process you believe in and can stick to, even under pressure.” – Howard Marks

The market environment in March and April presented a familiar but challenging pattern for investors in general and trend followers specifically: a sharp equity drawdown followed by an equally swift V-shaped recovery. Periods like these tend to expose the strengths — and weaknesses — of systematic investing approaches. For us, they have also served as a real-time validation of how our trend-following process has evolved over the years.

Historically, one of the common critiques of trend following is its tendency to lag during rapid reversals. A fast decline can trigger de-risking, only for markets to snap back before exposure is fully re-established. While that dynamic still exists to some degree in our portfolios because it is inherent in any rules-based, price-driven approach, our enhancements have meaningfully improved how we navigate both sides of that equation.

Refinement #1 - Using Single Stocks

One of the most important developments has been the refinement of how we express positions and exposures. When applicable and appropriate, we have embraced the deliberate use of individual securities rather than relying solely on market-capitalization-weighted ETFs. Broad ETFs, while efficient, can dilute the benefits of trend following by embedding exposure to both strong and weak components of the market. By focusing on single stocks, we are able to be more selective — leaning into leadership and avoiding areas showing persistent relative weakness.

During the March decline, this selectivity helped reduce exposure to the most vulnerable segments of the market. More importantly, as the recovery unfolded, it allowed us to reallocate toward stocks demonstrating the strongest momentum, rather than passively riding the entire index higher.

Refinement #2 - Expanding Alternatives Allocations

In parallel, we have expanded our use of alternatives trend- following allocations. These strategies, which may include non-traditional assets or differentiated signal constructions, provide an additional layer of diversification beyond equities. During periods of equity stress, they can behave differently — sometimes maintaining trends that are independent of the stock market’s direction.

In March, these allocations helped smooth the overall experience by providing exposure to trends that were either more stable or quicker to reassert themselves. As the equity market rebounded, they also contributed incremental return streams that complemented our core positioning.

Enhanced Adaptability

Taken together, we believe these enhancements have made our process more adaptive without sacrificing its core discipline. We are not attempting to predict turning points or outguess short-term market moves. Instead, we are continuously refining how we interpret and respond to price behavior. The goal is not perfection — no trend following system will capture every move — but rather, it is consistent improvement in how we manage risk and participate in opportunity.

The March episode is a good example of this progression in action. While the speed of both the decline and recovery tested all systematic investing approaches, our process was better equipped than in the past to navigate the volatility. By combining more robust signals, greater security-level selectivity, and diversified trend exposures, we were able to mitigate downside participation while remaining positioned to benefit as markets regained their footing.

Ultimately, this is the essence of our philosophy: evolve thoughtfully, stay disciplined, and let the trends — not predictions — guide the way forward.

Important Information:

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy or of any particular strategy or investment product. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. The above commentary is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Not intended as legal or investment advice or a recommendation of any particular security or strategy.

Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Miller Wealth Partners.