April 2026 Monthly Investment Update

Source: Blueprint Investment Partners

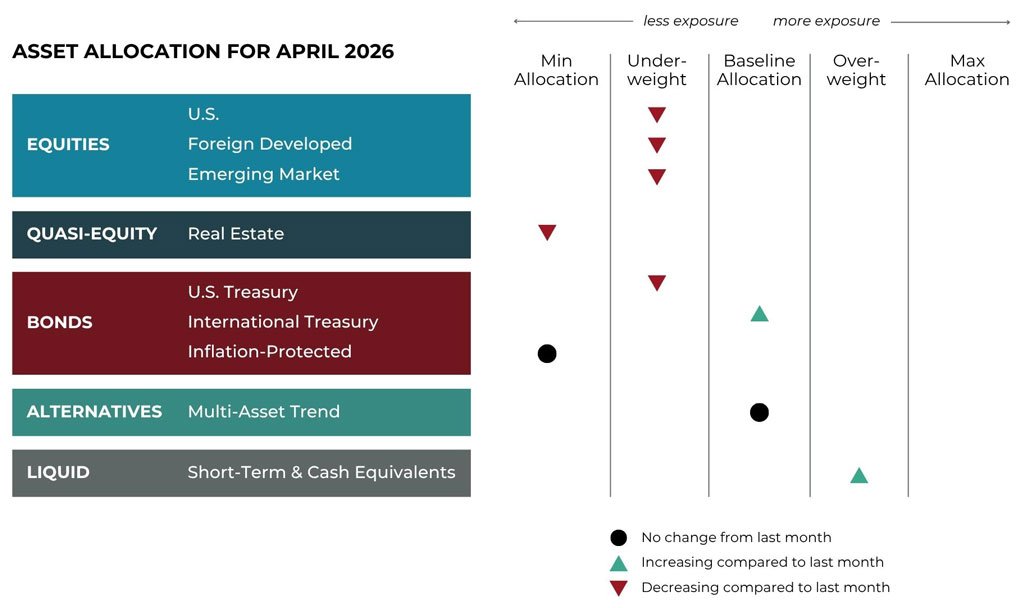

Adjustments can vary across strategies depending on each strategy's objectives. What's illustrated above most closely reflects allocation adjustments for the Growth Strategy. Diversification does not guarantee investment returns and does not eliminate the risk of loss. Diversification among investment options and asset classes may help to reduce overall volatility.

U.S. Equities

Exposure will decrease and move to underweight. The intermediate-term trend is now negative. The long-term trend remains positive.

International Equities

Exposure will decrease, with both foreign developed and emerging market equities now experiencing intermediate-term downtrends. Trends continue to be positive over the long-term timeframe.

Real Estate

Exposure will decrease back to the minimum allocation. With trends reverting back to negative status, it provides an opportunity to harvest losses while we await the next uptrend.

U.S. & International Treasuries

International Treasuries are now being partially expressed with an adaptive fixed income ETF. This will allow for an increase in exposure and offer the ability to potentially benefit from both positive and negative trends. However, U.S. Treasuries of medium to long duration are now in intermediate-term downtrends and exposure will decrease to underweight.

Inflation-Protected Bonds

Exposure will be at its minimum as it remains weaker than other fixed income assets.

Alternatives

Exposure is expressed through a multi-asset alternative ETF. Fixed income maintains its top spot in terms of exposure, but will experience a flip from net long to net short. Net long equities is the next-largest exposure and the top net long position, but the magnitude of net long will decrease. International currencies and commodities will bring up the rear in terms of exposure, with both continuing to be net long.

Short-Term Fixed Income

Exposure will increase to overweight as it takes on exposure from weaker equities and fixed income.

MONTHLY NOTE

A Disconnect Between Headlines & Market Behavior

“The essence of investment management is the management of risks, not the management of returns.”

– Benjamin Graham

Uncertainty can sometimes carry more weight than the event itself.

When headlines involve geopolitical tension or outcomes that are difficult to quantify, investor behavior often shifts quickly. Questions increase, confidence becomes more fragile, and long-term plans that felt stable weeks earlier can suddenly feel less certain.

Recent developments are a reminder of how quickly sentiment can change when visibility declines. The current environment is serious and evolving, but the underlying dynamic is not new. Markets have navigated wars, conflicts, and geopolitical shocks across decades, often experiencing short-term volatility while maintaining their longer-term trajectory.

This month’s Note looks at how uncertainty shapes investor behavior, why markets often move ahead of the headlines, and how we are adjusting exposure in response to changing market conditions—not in anticipation of them.

But first, here’s a summary of what transpired in the markets in March.

Asset-Level Overview

Equities & Real Estate

After mostly flattening since last Halloween, U.S. equities succumbed to the uncertainty driven primarily by geopolitical events, producing its first downtrends in almost exactly a year. In 2025 the uncertainty was also political and internationally focused, but it was tariffs and not war. Now with missiles flying in the Middle East and no clear end in sight, investors are rattled, which is leaving markets flat to down.

If there is a bright spot amidst this volatility, it is that the U.S. economy appears strong outside of inflation pressure. In theory, this would support a favorable environment if and when the conflict in Iran comes to a sustainable conclusion. The challenge is that if history has taught us anything, it is that tensions in that part of the world can linger for a very long time.

Foreign developed and emerging market equities became the undisputed market leaders in late 2025 and were holding onto that spot for early 2026 until things escalated in Iran. Now with their greater reliance on Middle East oil and closer proximity, markets in those regions have generally given back all of their 2026 outperformance. Like their U.S. counterparts, they now have intermediate-term downtrends. With no stronger equity asset class for this exposure to land in our portfolios, we will drop it all the way down in our quality curve to the historically safest landing spot: cash equivalents.

Real estate securities had finally managed to break out of their long sideways pattern and develop what appeared to be sustainable uptrends. However, like the other equity assets, uncertainty abroad has led to a collapse in share prices, leading to a return of downtrends. The result is that short-term losses will be harvested systematically and exposure will return to its minimum.

Fixed Income & Alternatives

With input prices on the rise, inflation is back to being a real risk to the economy. The result is rising rates and falling bond prices, especially among higher, more sensitive duration instruments. Our systems will respond by harvesting losses and cutting exposure, returning these allocations to ultra-short-duration cash equivalents.

Within the alternatives allocation, the sudden rise in rates across the globe has pushed fixed income prices lower and produced many short positions within the portfolio. Across both domestic and international Treasuries, positions will move to net short. The rise in volatility will increase the number of short positions within equities, but not enough to keep it from being the largest long position. Strength in the U.S. Dollar has cut international currency long exposure in half, but it will still outpace commodities, where shorts in grains remain but longs in metals and energy continue to dominate.

3 Potential Catalysts for Trend Changes

Diesel Prices:

The average price of a gallon of diesel recently rose above $5.20 nationwide, about 40% higher than a month ago. Most of the states with the biggest price jumps are in the Southeast, especially South Carolina, where prices have risen 51% since February 21. Higher diesel and oil prices affect the cost of many goods, and these increases have an impact on core inflation. For most freight companies, a 40% jump in diesel prices means their overall costs go up by about 10%. Diesel is used to run equipment in fishing, farming, and construction, such as tractors and cranes. While consumers may not notice higher prices right away, these costs are already moving through the supply chain. Companies that ship fresh food are hit harder because their products need to be kept cold and delivered quickly. This likely means farmers will start charging wholesalers more, and retailers who rely on these products will raise prices for shoppers. Companies that ship goods with less urgent demand may wait to send shipments until prices drop or use trains, which take longer but use less diesel.

Housing Update:

Mortgage rates have risen for the fourth week in a row, reaching their highest level since September. This sudden rise could slow down the start of the spring home-buying season. Freddie Mac reported that the average rate for a 30-year fixed mortgage is now 6.38%, up from 6.22%. Rates had dropped below 6% in late February for the first time since 2022, but have climbed quickly since then. The war in Iran and higher oil prices have led many to expect the Federal Reserve to keep short-term interest rates high for a while. This is tough news for the housing market, which has struggled for three years because of high prices and mortgage rates. Earlier this year, mortgage rates had fallen, and home prices were rising more slowly, giving buyers more choices and room to negotiate. Additionally, sales of existing homes went up in February as rates dropped. Zillow said that home-buying was more affordable in February than at any time since August 2022. However, as mortgage rates rise again, affordability is worsening, and the rapid increase may have scared off some buyers. The Mortgage Bankers Association said that mortgage applications have declined.

Consumer Services:

Strong consumer spending is pushing up the prices of services like haircuts and healthcare, making this a key issue in the Federal Reserve’s efforts to control inflation. Over the past year, attention was mostly on rising prices for goods and, more recently, on higher gas prices due to the war with Iran. However, the cost of services is a big reason why inflation remains above the Fed’s 2% target. Economists say service prices keep rising because people still have money to spend. Real wages are higher, and unemployment is low. Stock market gains have also made wealthy Americans even wealthier. According to Eugenio Aleman, Chief Economist at Raymond James, high-income households spend a lot on services like flights and restaurant meals, which keeps service inflation high. Services now take up more retail space than stores selling goods. In February, service prices excluding housing rose 3.3% year over year, a bit slower than in previous months. In the 2010s, the average yearly increase was 2.1%. According to a study by the Urban Institute, health insurance premiums through the Affordable Care Act’s marketplaces rose 21.7% this year from 2025, which is a much faster increase than in past years. The rise is due to expiring credits, uncertainty among insurers, and higher healthcare costs.

Sourcing for this section: The Wall Street Journal, “$5 Diesel is Crushing Truckers. It Will Soon BeFelt Across the Economy.,” 3/22/2026; The Wall Street Journal, “Mortgage Rates Rise for Fourth Straight Week,” 3/26/2026; and The Wall Street Journal, “America’s Sneaky Inflation Culprit: Manicures, Haircuts and Doggy Daycare,” 3/23/2026

Emotional Investor Reactions Are Usually Riskier Than Perceived ‘Risky’ Events

“Far more money has been lost by investors preparing for corrections, or anticipating corrections, than has been lost in corrections themselves.” – Peter Lynch

Markets don’t operate in a vacuum. Headlines matter — especially when they involve war, geopolitical tension, or uncertainty that feels difficult to quantify. And if there’s one thing we’ve been reminded of time and again, it’s that uncertainty — not necessarily the event itself — is what tends to unsettle investors the most. When geopolitical conflict escalates, the instinctive reaction is often fear. Clients call. Long-term plans suddenly feel less certain. The narrative becomes, “This time is different!”

Markets have endured wars, conflicts, and geopolitical shocks across decades. While short-term volatility is common, the long-term trajectory has often remained intact. In many cases, markets begin recovering well before the underlying conflict is resolved. That disconnect — between headlines and market behavior — is where many investors get tripped up. The real risk is often not the event itself, but the behavioral response to it.

Avoiding uncertainty may feel prudent, but without a plan for how to do so it may lead to jumping the ship too early or missing the recovery that follows. And that recovery rarely comes with a clear signal that “it’s safe to get back in.” By the time uncertainty fades, markets have frequently already moved higher to a point making the re-entry emotionally difficult.

That said, acknowledging history doesn’t mean ignoring risk. This is where investing process matters. Rather than trying to predict geopolitical outcomes — or guess how markets will react — our firm relies on a disciplined, trend-following approach. Trends allow us to observe what markets are actually doing, not what we think they should do. When uncertainty rises and trends deteriorate, our investing process naturally reduces exposure to risk assets. You see this playing out in real time, as we are reducing U.S. equities exposure due to deteriorating trends heading into April.

Importantly, this is not about reacting to headlines. It’s about responding to price behavior. As trends weaken, we systematically reduce exposure. Not because of any single event, but because the market itself is signaling increased risk. We think this approach helps us avoid making emotionally driven decisions in moments when emotions are running high.

The other side of this discipline is just as important. We remain equally prepared to add exposure back. If uncertainty begins to abate and markets rebound, trends will reflect that improvement. And when they do, our systematic investing process allows us to increase exposure again — without hesitation and without needing to “feel comfortable” first.

This is one of the key advantages of a rules-based approach, in our view. It removes the burden of prediction and replaces it with a repeatable framework for decision-making. In environments like today, that matters. Because the reality is that uncertainty is always present. War may dominate headlines today; tomorrow it could be inflation, central banks, or something entirely unexpected. The specific catalyst changes, but the underlying challenge for investors remains the same: how to stay disciplined when uncertainty is high.

Our answer is simple. We don’t try to predict. We don’t react emotionally. And we don’t assume that “this time is different.” And throughout, our goal remains consistent: to participate in markets when conditions are favorable and to step back when risks increase. History doesn’t eliminate uncertainty — but it does provide perspective. We think investing process turns that perspective into action.

Important Information:

Past performance is not indicative of future results. The material above has been provided for informational purposes only and is not intended as legal, tax, or investment advice or a recommendation of any particular security or strategy or of any particular strategy or investment product. The investment strategy and themes discussed herein may be unsuitable for investors depending on their specific investment objectives and financial situation.

Opinions expressed in this commentary reflect subjective judgments of the author based on conditions at the time of writing and are subject to change without notice. The above commentary is for informational and educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Not intended as legal or investment advice or a recommendation of any particular security or strategy.

Information obtained from third-party sources is believed to be reliable though its accuracy is not guaranteed.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission from Miller Wealth Partners.